Have You Seen The Dead Walking?

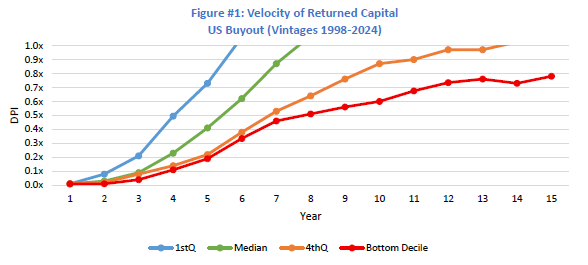

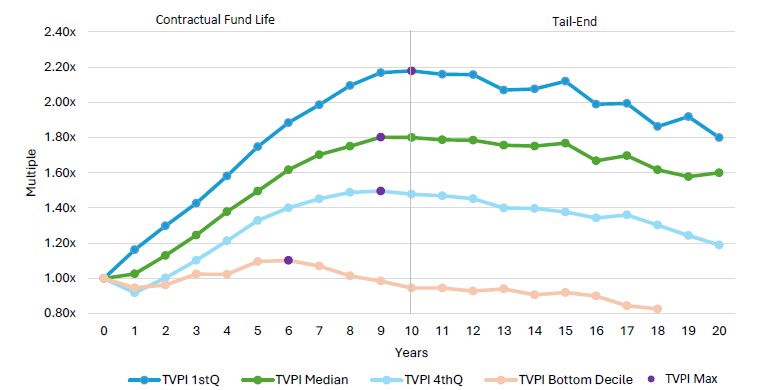

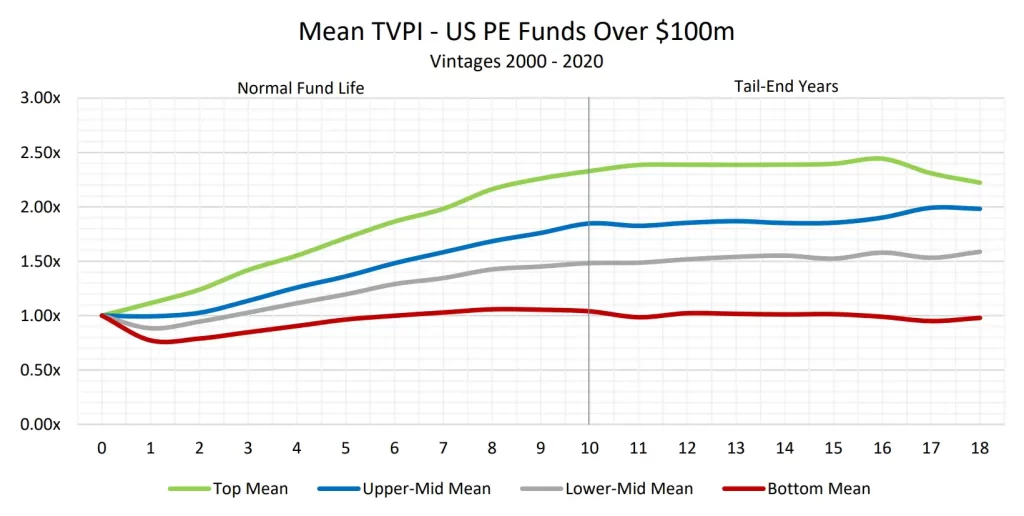

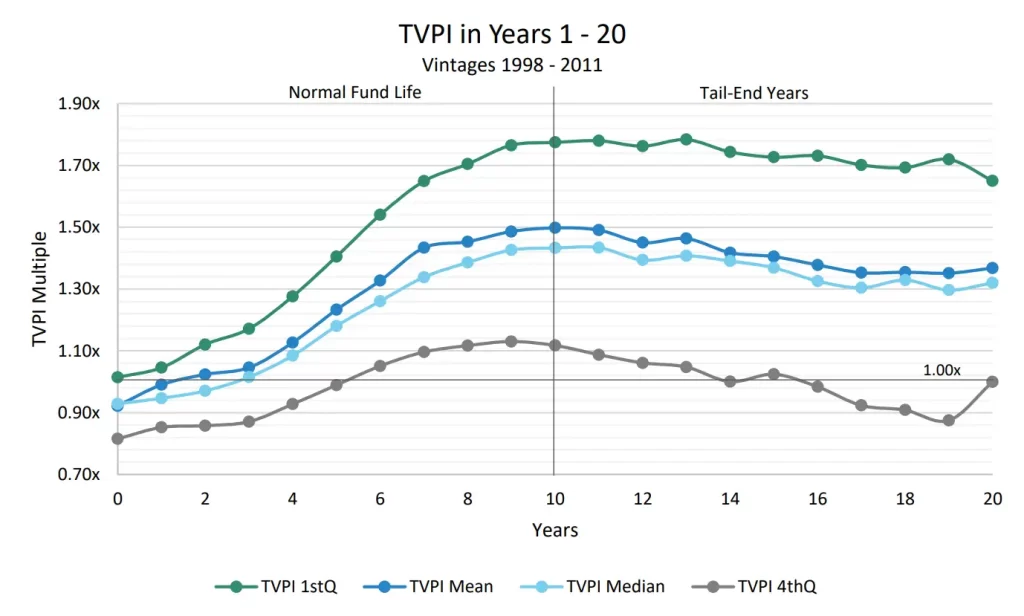

Continuing on our previous research, this white paper provides context on the growing universe of zombie funds and, importantly, the key metrics that LPs can utilize to identify them. Specifically, using data on US buyout funds from 1998 to 2024, we provide context regarding timing of liquidity and the Realization Ratio (DPI/TVPI Max) as it relates to fund performance.

We estimate that there are over 500 active zombie funds, taking into account both fund performance and key manager metrics. We use both criteria versus simply defining a zombie as any single underperforming or aged fund.

In addition, the report provides a set of solutions that guide investors on steps to mitigate potential future losses associated with such managers.